Disclosure: Please note that I may benefit from purchases made through my affiliate links below, at no cost to you. Additionally, as an Amazon Associate, I earn from qualifying purchases. Thank you for your support

Oops, it’s nearly the end of July as I write this “mid year” review of 2022 goals. But as I didn’t set my goals for 2022 until February … I think it’s just the right time to do a review!

I’m writing in my attic room as the sun is setting – I can just glimpse the orange glow from the corner of my eye. I’m in London on a 4.5 week holiday. My first overseas holiday in 3 years.

After an epic 17 hours 15 minutes non stop flight from Perth to London (in addition to a 4 hour flight from Melbourne to Perth earlier with an one hour transit in Perth airport), I arrived as dawn was breaking on Thursday. Phew, tested negative upon arrival. But 24 hours later, I was coughing and spluttering and yes, tested positive to Covid.

This is really ironic. I’d splurged on premium economy seats using my Qantas Frequent Flyer points (amassed from not travelling for 3 years) so there are less people in my vicinity. I chose the long direct flights because I didn’t want to transit outside Australia.

But the rules had changed just before my flight. Passengers need not be vaccinated nor do we need a negative test to board. Masks were mandatory from Melbourne to Perth but not on the international flight from Perth to London. The vast majority of passengers, including the guy next to me did not wear a mask.

I’m blaming the 17 hour flight. Even though I wore a mask throughout the flights (and changed the masks a few times), it wasn’t enough. I always knew the possibility that I’d catch Covid on this trip and brought medicines with me for symptomatic relief. But I thought I’d catch it from gallivanting about in London, not from the flight over.

Anyway, this enforced rest with lots of sleeping and reading will prepare me for lots of adventure ahead.Thank goodness for the Libby app – I have access to thousands of books from the two libraries I’m a member of in Melbourne. I’ve already read 5 books.

But I am frustrated at missing out on a family outing to see The Jungle Book at Kew Gardens and having to cancel a lunch with Sam (Late Starter to FI Series #2) in Bath. I was so looking forward to meeting up in person.

The silver lining I suppose, is that it’s now out of the way and I can enjoy the rest of the holiday without worrying about when I’d be getting it.

I’ll be posting my shenanigans in the UK on my Instagram and Facebook ‘stories’ if you’re interested in following along 🙂

All right, now that you’re up to date with my Covid status, how have I been travelling in 2022? Am I any closer to achieving my goals?

Feeling Overwhelmed?

Use this FREE Checklist to start your journey to Financial Independence

Goal 1 - Invest $30k into my Shares Portfolio

So far, up until today, I’ve invested $18492 so I should be on target here. Even though this is on auto pilot, I’ve had to review my weekly amounts as I transition to working 4 days a week. It is still my absolute priority though to invest $30k this year.

And yes, the share market has been rather volatile in the last seven months but I can’t control that. I can only control how much I invest in it.

Goal 2 - Rebuild my Emergency Fund

I raided my Emergency Fund last year to replace major appliances when they broke down plus some home maintenance expenses. It’s slowly being rebuilt.

I feel secure with holding 6 months’ of expenses in it and I’m up to 5 months now.

I stopped contributing to it for a month or so in order to build up one month of expenses in my Bills account so that I would always have enough to pay next month’s bills. The anticipation of reduced pay from working 4 days a week brought up some feelings of insecurity.

Goal 3 - Make a Will

I won’t lie. This was very challenging. And confronting. I wrote about it – What Happens if You Die Tomorrow? How to Make a Valid Will.

But after my lawyer sent me all the paperwork for review, the thick pile of papers just sat on my dining table. For MONTHS.

Then everything kind of happened to make it all come together.

There were two close family members’ deaths within my circle of friends. It suddenly brought home to me again how crucial (and kind) it is to leave clear instructions for the people left behind.

And it became clearer who my people should be – the executors of my will, attorneys for Enduring Power of Attorney and Medical Treatment Decision Makers.

I had dragged my feet for months, not wanting to initiate a conversation with them and asking their consent to take on the specific role.

With my overseas holiday looming, suddenly everything needed to be in place. And it was easier than I had imagined. All said yes, thankfully! And it was then just meeting with my lawyer one more time to get final documents plus obtaining everyone’s signatures.

I’ve also sent off my binding death benefit nomination to my superannuation.

So I can say that this goal has been achieved! Woohoo!

It really does feel good (and a weight off my shoulders!) to have all these estate planning documents in place. There are now instructions for what to do when I’m dead AND what to do if I’m alive but incapacitated (which is the scarier option, to be honest).

Goal 4 - Make Health & Wellbeing a Priority

I have lost 1kg out of the 5kg I wanted to lose.

I started off quite well early in the year, walking for at least 20 minutes every morning before work. Then I had a terrible cough that everyone thought sounded like a Covid cough. But several RATs and a PCR test confirmed it wasn’t due to Covid, influenza or RSV. So no one knew what it was from but all concluded I needed to rest. The weather became colder and I stopped going out in the mornings.

I plan to walk every day when I’m on holidays so I’m hoping to kickstart the habit again. (It hasn’t happened yet, holing up in my attic room!)

Besides March when my savings challenge involved me paying myself $5 a day if I didn’t eat chips or chocolate but penalising myself $10 if I did, I wasn’t very controlled in my snacking habits.

I’m trying to learn not to be an “All or Nothing” person. My word for 2022 is Consistency and it is this area that I need to apply it most. I have been consistently inconsistent in my prioritising of health and wellbeing.

I prioritise it when I’m in pain and then forget when I’m not. For example, I have consistently seen a massage therapist and osteopath to keep my shoulder pain under control. And now I also have jaw pain due to all the jaw clenching in my sleep.

But what I really need to do is to prevent the pain in the first place. That will be the goal for the next 5 months.

Goal 5 - Prepare for the Non Financial Aspects of Retirement

I read 2 books to help me with this goal – How to Retire Happy, Wild and Free by Ernie J Zelinski and Keys to a Successful Retirement by Fritz Gilbert – I reviewed them both plus Retirement Made Simple by Noel Whittaker which I read last year.

All emphasised preparing for the non financial aspects – in particular, finding purpose in retirement. I’ve started lists based on the Get-a-Life Tree illustration in Zelinski’s book.

My travel list is by far the longest among the lists of activities I can pursue. And while I’m on holidays, I’ll indulge in what I know has brought me joy in the past – exploring new places, eating good food, seeing live theatre, visiting museums and galleries plus spending time with my family. Just to confirm that they still bring me joy, haha!

FIRE Progress Update

There are 5 metrics that I track on the way to FIRE and here is their progress in the first 6 months of the year.

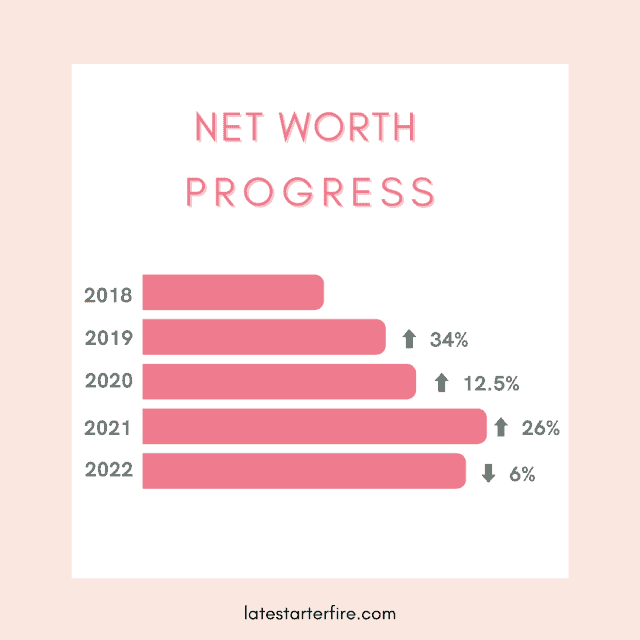

Net Worth

The above chart shows that my net worth fell by 6% compared to the end of Dec 2021. This is totally expected due to the volatility of the share market. I am not too concerned about it. This net worth figure does not include my paid off house which I have no intention of selling in the near future.

Bridge the Gap Fund

My goal is to retire at 55. This means I need a Bridge the Gap fund to support me for 5 years before I can access my superannuation (retirement fund) at 60.

My Bridge the Gap fund is comprised of my shares portfolio and cash. Right now I’m focusing on investing as much as I can into the shares portfolio and have not started accumulating cash.

It has only fallen 0.6% compared to the end of 2021 so I’ll just be consistent here and stay the course.

Superannuation

How is my retirement fund going since it is what I will rely on once I turn 60?

The balance as at the end of June 2022 was 8.7% less than the balance at the end of December 2021. Once again, this was expected due to market volatility. Since I haven’t sold anything, this is only ‘paper’ loss. Hopefully, the next nine years will see a return to growth.

And the balance is still higher than the balance when I declared I was at Coast FI in April last year.

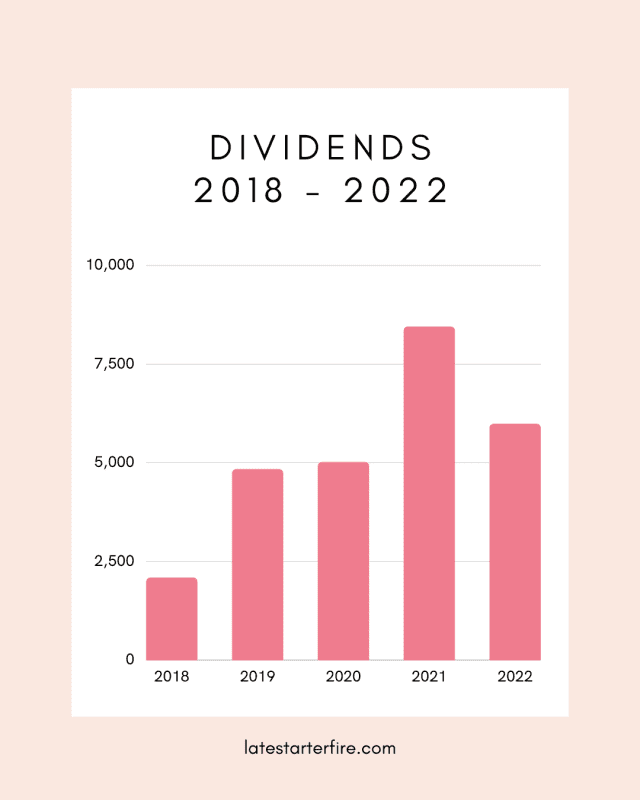

Dividends

Dividends is hands down my favourite metric to track!

So far, the first 6 months of 2022 has been stellar – dividends received are equivalent to 72% of total received in 2021.

My aim is for dividends to support half my expenses by the end of 2026. It’s at 30% of achieving this goal so a fair way off yet.

Expenses

2022 has been kinder than 2021, mainly in the absence of failing appliances and home maintenance.

So far, I’m on track to spend less than $40k this year but of course, not all my holiday expenses are part of this progress report. I can already tell you that July and August will be much more expensive than the previous two Covid years!

Final Thoughts

I do love this time of year as a second chance to refocus where I need to and to celebrate if I’ve achieved a goal.

After this review, I need to stay the course financially and I should be on target to achieve my goals for 2022.

Where health and wellbeing is concerned, I need to refocus my energy on preventative measures. Otherwise I’d be spending heaps on osteopath treatments and remedial massage. Plus not able to keep my weight down. Wealth without health is useless.

And I’m totally celebrating achieving and exceeding one goal ie estate planning done instead of just making my will. Yay!

)

)