Disclaimer – I am not a lawyer, financial planner or accountant. The following is my understanding of how wills and estate planning works. I am sharing the process I took. Each state and country has their own laws governing wills and estate planning. I am writing as someone living in the state of Victoria, Australia. Please seek your own legal, financial and tax advice

Making a will is one of my 2022 goals.

How have I lived till 50 and not made a will??

Several reasons.

(1) I am single and have no dependants. So I never think it is a priority. Who cares if I’m dead?

(2) I don’t have many assets – I have nothing to leave anyone

(3) It’s too daunting and overwhelming a process – where do I even begin?

(4) I don’t want to think about my own demise

(5) It seems like a ‘too adult’ thing to do!

But … being on the path to Financial Independence has changed my mindset on making a will.

Because I do have assets now, after nearly four years on the FI path – a paid off home, growing shares portfolio and superannuation.

And when you have assets, you need a will. Full stop.

Because a will is essentially a legal document that sets out your wishes for what to do with your assets after you’re dead.

I didn’t think I cared much about what happens to my assets after I’m dead.

But it turns out that I do.

If you die without a valid will, the state decides how to distribute your assets. There is a set formula that considers your spouse, parents and dependants. If you don’t have any of them, your assets go to the state.

I’ve worked hard to build my assets. And at the end of the day, I’d like a say in how they are distributed. It would also make my loved ones’ lives easier if I leave clear instructions. And I would like to leave a meaningful legacy to the next generation if possible.

Feeling Overwhelmed?

Use this FREE Checklist to start your journey to Financial Independence

What is a valid will?

A will is a legal document. And is valid if the following are fulfilled.

You must be of sound mind to make a will. That is, you must be able to understand what you are doing.

And not have done it under duress from another person.

You must be over 18 years old.

It must be in writing and intended as your will.

It must be signed by you in the presence of at least 2 witnesses and dated at the time of signing.

How to make a valid will

I explored 3 options on how to make a will – online will kit, State Trustees and an estate planning lawyer

(1) Online will kits

It’s very affordable and the process is simple. Fill in a questionnaire, submit for review and you get a written document; sign it (with 2 witnesses presumably) and keep it somewhere safe.

But in the end, I decided I needed more guidance and advice about my own situation. I was also concerned with how legal it is and did not want any hassles for the people left behind.

(2) State Trustees

This is another alternative as a low cost option. Thanks to @adultingworld on Twitter who suggested this option. I knew they can be appointed as administrators and executors but did not realise they had a will writing service.

It is a state government owned company – the are the Public Trustee of Victoria. Each state has their own service.

In my professional life, I have to deal with them. And felt they were too giant of a behemoth to interact with on a personal level. But they do have good information on their site.

(3) Estate planning lawyer

Rejecting the first two options means that I am now looking for a lawyer.

Googling estate planning lawyer in my area turned up a few names but I didn’t have much luck when I looked them up. Either because I didn’t relate to their profiles or the firm was too big and intimidating. After all, it’s not as if I have a great fortune or millions for anyone to fight over. Another one took weeks to email me a questionnaire.

I was about to give up when an Instagram friend who writes at iambuildingwealth.com recommended Head and Heart Estate Planning. I checked out her Instagram feeds and website, liked what I saw and booked a free 15 minute discovery meeting for the next morning.

And thank goodness, Lucy was very down to earth, answered all my questions which took longer than 15 minutes. Most importantly, I didn’t feel intimidated or stupid. She explained it in terms I understood and asked me thought provoking questions.

I can’t stress quite enough that making a will and going down the estate planning path is scary and confronting. Having someone you can relate to and who can guide you through the process is priceless.

Lastly, I don’t think anyone will contest my will. But I aslo can’t predict the future. So it’s for my peace of mind to have a proper will done with a specialist estate planning lawyer. There’s an excellent post about wills being contested on Money School.

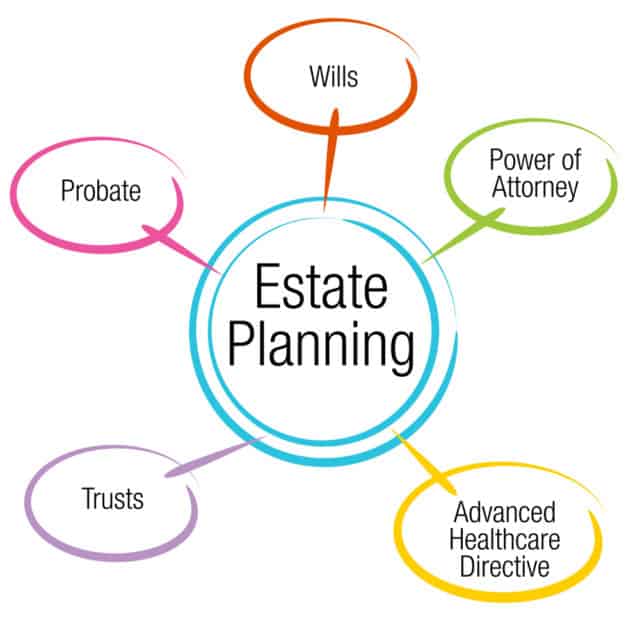

What is estate planning?

I also didn’t know the difference between making a will and estate planning. I thought making a will was enough. But a will only looks after your assets when you’re dead.

What happens if you are still alive (eg after a stroke, dementia, accident) but can;t look after your own affairs?

That’s where an estate plan comes in – it provides for what to do after you’re dead (ie having a will) AND while you’re still alive but incapacitated (ie Power of Attorney for financial and lifestyle plus appointing a medical treatment decision maker).

And all of a sudden, the decisions and things to consider just compounded!

So now, not only do I have to think about what happens after I die but also who I’d like to appoint to make decisions about my finances, lifestyle and medical issues if I’m incapacitated for whatever reason.

Questions and issues to consider when making a will

I will deal with the after death issues here and leave the before death issues to a separate post. The following is not meant to be an exhaustive list but these were the questions and issues I worked through with my lawyer.

Time frame

I was very confused about the timeframes. I kept thinking that there’ll be hardly anything left of my assets if I were to die in 20 or 30 years.

My lawyer very nicely pointed out – “No, no – we are talking about what happens if you die TOMORROW.”

🤯

Well, that was confronting! But it also brought clarity.

I don’t need to worry about what happens in 30 years – I just need to think about now and my current assets.

What are your current assets and liabilities?

You will need to list your current assets and their value. Plus any life insurance you may have, including the one in your superannuation.

I had no issue with this question because I track my net worth every month 🙂

This is also where you consider if you have any special possessions eg jewellery that you want to bequeath to certain people.

And income from a business or royalties from creative work etc.

How will you distribute your assets?

Who are your beneficiaries ie who will inherit your assets?

They can be organisations such as charities or schools or individuals.

If you are leaving assets to the next generation, consider if they are yet unborn. Will you, your siblings or cousins, for example, have more children? In an ideal world, you die after you’ve just updated your will but that may not be the case.

You can structure your will in layers as my lawyer describes it. For example, if my parents are still alive at the time of my death, I want them to tp be taken care of first before the other beneficiaries. But if they are deceased, then it can go to blah blah. And if blah blah is deceased, it can go to another person. And so forth.

Are your beneficiaries minors?

If they are minors now, what are your intentions?

Are you happy for them to inherit the money while they are minors? Or would you like them to have control at a more mature age? And what would that age be?

And if they are your children, who will look after them until they turn 18 ie who will be their guardian(s)? How will you provide for their guardian(s)?

How can you protect your assets for your beneficiaries?

Unfortunately in our society, divorce and relationship breakdowns are more common than not. Will your beneficiary lose half their inheritance should their relationship break down?

Do you care how your money is to be used?

Do you want to specify how that money is to be used? For example, do you want the bulk of the estate left for the following generation and that this generation can use the income only? Or perhaps specify how the income should be used, perhaps for the education of the beneficiary while they are still minors? Or should the income be reinvested only?

The possibilities are endless.

Although it’s tempting to exert control from the grave, maybe it’s better to just let it be and let your beneficiary deal with their inheritance as they see fit. And also not bound the trustees too much as they carry out their duties and allow them some flexibility.

Who will be your executor?

An executor is the person you appoint in your will to carry out your wishes as stated in the will upon your death.

It doesn’t have to be a person you know. It can be a professional executor or a company such as the State Trustees.

If it is someone you know, it should be someone you trust to carry out your wishes. It can be a huge undertaking. There will be many tasks starting with finding your will and organising your funeral, informing organisations you deal with of your death, selling properties and so on.

Are they competent or have the correct skill sets to do the job? Will they have time to do it properly? It may take years to settle a complicated estate.

You can appoint more than one executor. Or have executors as back up in case the first one is unable or unwilling to accept the job. But they will need to be able to work together. How will decisions be made?

And one of the executors must be an Australian resident for tax purposes as they need to file your final tax return and sign on your behalf. If your executor lives overseas, they cannot fulfill this obligation even though they may be Australian citizens.

Will you pay your executors a fee for performing the role? Or will you ask them to do it for free?

Testamentary trust

Consider setting up a testamentary trust if you want to protect the assets for your beneficiary. The trust only comes into effect upon your death. All your assets are then owned by the trust.

This is where you can specify how the income from your assets should be distributed. Who has access to this income? What can the income be used for?

The trust must have trustee(s) who look after the assets and carry out your wishes. Once again, consider the skill sets of the people you appoint as trustees. And whether they have the time to do all the tasks.

Once again, do you pay your trustees? Or will they do it for free?

There are other uses of a testamentary trust but I will be using it because my beneficiaries are under the age of 18 right now and I don’t want them touching the assets until they are 30 years of age. Yeah, I know – I am a mean aunty.

Superannuation

Wait for it – the money in your superannuation is not part of your estate unless you have a binding death benefit nomination in place.

If you don’t have one in place, the Trustees of the superannuation fund decide who gets your money. Even if you’ve nominated certain people when you first joined the fund – these are non binding.

There are only certain people in your life who are deemed suitable to receive your superannuation. They must be a child, spouse or dependant. So I can’t leave it to a niece if that niece is not my dependant. I also cannot nominate my parents.

And this is where I get mad and think it is discriminatory towards single people. We have no choice but to nominate a legal personal representative who will then instruct that the superannuation benefits be part of our estate.

In addition, these binding death benefit nominations only last 3 years and must also be updated when circumstances change. The fund I’m with doesn’t provide an option for a longer timeframe. It is very frustrating!

The binding death benefit nomination forms can usually be downloaded from your superannuation’s website.

What happens if EVERYBODY you've nominated as your beneficiaries dies?

Should a tragic catastrophic event happens and all your beneficiaries die with you – who will inherit your assets?

This question also blew my mind. Now not only am I dead but so are all my loved ones!

My lawyer suggested that I think of some other people in my community or charities that can benefit from my assets. And stipulate percentages to each entity.

When should you update your will?

Wills are not a set and done ‘chore’. They need to be amended when circumstances change, for example if anyone named in your will dies before you; if your relationship status changes; if your assets change – you may dispose of an asset etc

I will add reviewing my will and checking my superannuation binding death benefit nomination to my annual financial checklist.

Final thoughts

That sounds ominous for this particular post!

Jokes aside, making a will can be confronting and overwhelming as we think about how we’d like to provide for our loved ones after our demise. And if we don’t have any loved ones, we can leave our assets to our favourite charities or other organisations that may benefit from our hard work.

There are so many questions, issues and scenarios to consider when making a will. I confess I needed a lie down after my first call ended with my lawyer.

The truth is that I do have assets after nearly four years on the path to financial independence. I do want to have a say in how they are distributed after my death. And I don’t want to leave a mess for those left behind. I also don’t want the will to be contested. And therefore have chosen to work with a specialist estate planning lawyer.

It is a worthwhile process.

Here are some resources if you wish to learn more about making a will and estate planning –