I do love setting goals at the beginning of the year. It gives me something to work towards for the next 12 months, signalling a hopeful and new beginning. Anything is possible!

And it builds on what was achieved in 2021.

January was tough for me, physically and mentally due to a stressful workload and difficult conditions at work. Thank you, Omicron. But that is behind me now.

And really, it’s NOT too late (that IS my message as a late starter 🤣) to set my goals for 2022 – it’s only the second week of the Lunar New Year!

I also want to try something new for 2022. New to me, that is.

I was inspired by Gretchen Rubin’s podcast episode on choosing a ONE word theme for the new year.

And so I will choose a one word theme for 2022. A word that will guide my actions and when life happens, I’ll just come back to this word to right the ship again.

🥁 My one word is CONSISTENCY.

It’s a boring word, to be sure.

But quite honestly, I’m tired of the stops and starts I’ve had in all areas of my life. I just want to be CONSISTENT and keep at it. Stay the course.

I also know ahead of time that I will fail at it. But I want to then get up and get back on he horse again immediately instead of beating myself up.

What are my goals for 2022 with the word Consistency in mind?

Feeling Overwhelmed?

Use this FREE Checklist to start your journey to Financial Independence

Goal 1 - Invest $30k into my shares portfolio

Stay the course.

I did this for 2021 and I will continue to invest $30k into my shares portfolio for 2022.

My retirement date is set for 31 Dec 2026. That is 1786 days away or 58 months of work left. I will be 55 and a few months old.

My original plan to fund the 5 years before I can access my superannuation (ie from age 55 to 60) is to sell down my shares portfolio every year. And have one to two years of living expenses in cash, just in case the market isn’t cooperating at the time I retire.

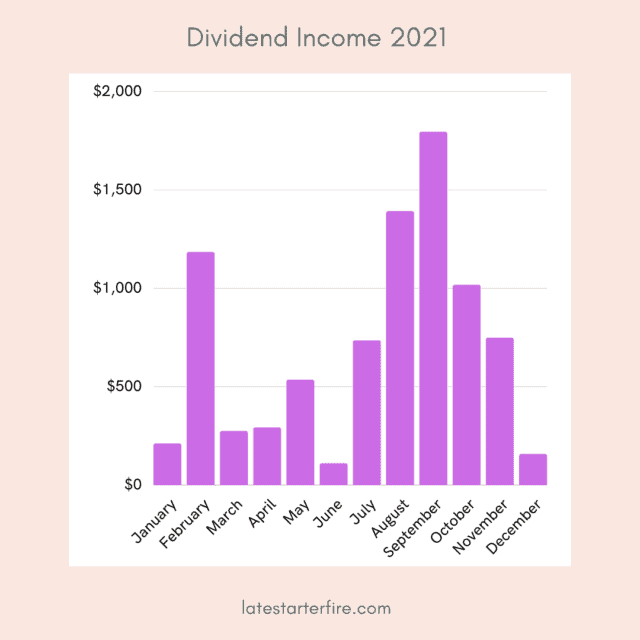

However this plan has evolved. All because I started tracking my dividends as an exercise to track passive income in 2021.

Before 2021, I had no idea how much my dividend income was because the majority was reinvested immediately via Dividend Reinvestment Plans (DRPs). Cash did not hit my bank account so I was oblivious. Out of sight, out of mind.

So I was pleasantly surprised by the result.

I started to think that perhaps I won’t have to sell the entire portfolio. I could live on the dividends and make up the rest with cash. Unfortunately as a late starter, I just don’t have the timeline to have a big enough portfolio to live off its dividends alone.

By the end of 2021, my dividends were at 42% of my target for retirement. This target is based on half of my projected annual living expenses. It would be awesome if this target is exceeded – that would mean I need to save less cash.

So I’m giving myself two years to invest as much as I can into this shares portfolio. I will then reassess the dividend income and determine how much cash I need to save. At this stage, my plan is to save up to 2 years of living expenses in cash regardless. I will have 3 years to do so.

I can always revert to my original plan to sell down the portfolio if Plan B doesn’t work. Or at least sell off the individual shares I own and keep the ETFs and LICs. Based on my original plan, I’m at 77% of my target portfolio value.

We’ll see – it’s all a big experiment 😬

Goal 2 - Rebuild my emergency fund

This was impacted by my horror year of home maintenance costs in 2021. Once again, I will stay the course and continue to build it back up to 6 months of living expenses. It will form part of the 2 years of living expenses I need at the start of my retirement.

Goal 3 - Make a will

I can’t put this off any longer. It just seems such a daunting undertaking.

How do I find a lawyer? What do I have to consider besides who to leave my assets to if I get hit by a bus tomorrow?

So 2022 is my deadline to make a will and set up binding death benefit nominations in my superannuation. Sounds ominous!

Goal 4 - Make health and wellbeing a priority

This is where I need consistency the most.

The money goals are much easier to achieve now that I’ve been pursuing Financial Independence (FI) for three and a half years. Most of my saving and investing are automated anyway so I just have to review them every now and then to make sure I’m still on track.

But prioritising self care is HARD. It can’t be automated, sigh.

By self care I mean taking care of my physical and mental health.

I still want to lose 5kg.

So I need to eat better, snack less often and learn to de-stress without resorting to chips and chocolate. I have to stick to my daily stretching and exercising. How on earth will I run a marathon or hop on and off little boats in Antarctica (both decade goals) if I am unfit? Oh and sleep better – so I am rested and rejuvenated to start the day energised.

As I age, my healthcare costs will only increase, as evidenced by my 2021 expenses. My medical category (which includes osteopath treatments, remedial massages, GP visits, psychologist, pathology, medical procedure etc) was the fifth biggest category at 7.9% of total expenses. So it is time to make sure I take care of myself and lower this cost.

Goal 5 - Prepare for the non-financial aspects of retirement

The financial aspect of my retirement plan is under control as I’ve spent the last three and a half years focusing on it.

It’s time now to explore the non-financial aspects.

What will be my purpose in retirement? What activities will I start exploring now? I have started to jot down ideas for travel – this list will be very long!

And as part of this goal, I want to prioritise activities that bring me joy and do more of them in 2022. This way I won’t be at a loss when I finally retire. None of that ‘but what will I do if I retire?’ dilemma here.

Final thoughts

I know the last two goals are a bit iffy – how will I know if I’ve achieved them?

For goal 4 – I will feel better physically and mentally

And goal 5 – I will have lots of activities written down. And I will document my progress on Instagram as I explore activities throughout the year. Follow me on Instagram to check out my progress and keep me accountable 🙂

Anyway, my real goal is to be consistent in pursuing these activities. The very act of putting my goals here will hold me accountable.

Plus the most valuable lesson I learnt in 2021 was that taking small steps in the right direction was better than not taking any steps at all.

I’m excited for more progress in 2022!