An annual review is never complete without an expenses review,

The good news is that I spent 6.5% less in 2022 vs 2021.

And that is despite travelling overseas and indulging in expensive dining experiences.

So my top 5 spending categories in 2022 were:

1. Travel at 21.6%

My overseas holiday in July was funded by my Travel sinking fund – money I’d set aside consistently every week from my pay. This is my true guilt free spending account. Everything that I spent during my holiday was categorised under Travel, be it food or transport or anything else.

Also, in December, I paid for return airfares to London via Singapore for next July.

2. Financials at 16.6%

This is mainly professional fees and insurances associated with work plus estate planning lawyer fees.

3. & 4. Food and Health & Wellbeing equal tie at 13.5%

My biggest food month was in December because I had overseas visitors staying with me plus there was Christmas lunch

. I enjoy food and show love via cooking so food will always be a top spending category.

. I enjoy food and show love via cooking so food will always be a top spending category.

Due to TMJ pain, I’ve been visiting the osteopath more often. And also a massage therapist for sore shoulders during the first half of 2022.

5. Personal at 7%

Besides personal hygiene items and haircuts, I dump everything in this category that I don’t know what to classify under. So this year it included my Apple macbook! It was one of my favourite purchases this year so no regrets 🙂

I did spend more than what I’ve been budgeting for future retirement expenses (17% extra!) so it’ll be interesting to see if expenses for 2023 can be pared back a bit. This extra 17% accounted for the Apple macbook, return air fares to London for July 2023 and estate planning lawyer fees.

All in all, 2022 has been a very full year for me.

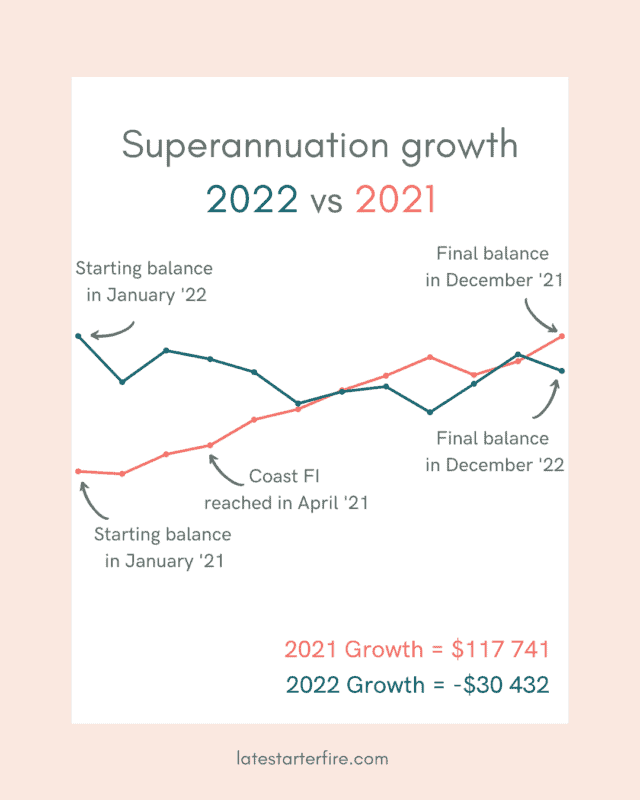

Financially, it doesn’t look so good in that superannuation balances and my shares portfolio both fell in value. But my dividends improved and can cover 35% of my projected retirement living expenses. There is good news among all the bad news!

What I’m most happy about is the non financial aspects – finally having an estate plan in place, prioritising my mental health, working 4 days a week and rediscovering what I love doing and who I love spending time with.

Thank you, 2022 – it’s time to say farewell as I look forward to 2023

I’m going to London in 2023 too – but I’ll be there in September for 5 weeks.

Isn’t it great to be able to travel again?

Oh, it’s sooooooo good to be able to travel again! I’d forgotten how good it was until the plane lifted up into the clouds – bliss. Enjoy London! It’s one of my favourite cities in the world