Disclosure: Please note that I may benefit from purchases made through some of the links below, at no cost to you.

Investing.

The word brings chills down my spine.

It is a world of unknowns, a mysterious realm.

Especially when you don’t work in the finance industry or has had any education about the finance world.

When your financial literacy is gleaned from your mother’s teachings based on her mother’s experiences.

Recently, I read an article which struck a chord with me – “Why is it important for women to invest and not just save?” from Women Who Money

This was my instinctive reply on Twitter –

It is intimidating to invest when you are afraid of losing it and not having time on your side to correct any mistakes https://t.co/iSQ1cHVchO

— Latestarterfire (@latestarterfire) May 24, 2019

What if you start investing late in life?

It’s such a conundrum – you don’t earn very much when you start working. So you don’t think you have enough money left over from daily living expenses to invest in anything. Then when you do start earning more money, you succumb to lifestyle creep and you still don’t have spare money to invest.

Because I am starting late in my 40s, I constantly feel I am behind. I am anxious that I will not have enough for my retirement, traditional or otherwise.

This anxiety makes me want to rush in and buy into anything that will give me a great return.

But the same principles still apply. Whether you are investing in your 20s or your 40s.

Know thyself

I need to know myself – what sort of risk can I tolerate? In investment language, the higher the returns the higher the risk. Will I sleep at night if my share portfolio is not doing well?

How worried am I that I will lose the money? Is it a justified worry? How will I mitigate these risks? My mother always advises me not to put all my eggs in one basket. So is there a way for me to spread the risk?

How much time do I have for this investment? What is the recommended time frame? When do I want to use the money invested?

Do I understand the investment vehicle? If I cannot explain it to a friend over a cup of coffee, then I will not invest in it. (That is my my very basic yardstick!)

I understand that compound interest works best when you are young and have many years ahead. But it sill works in your 40s if you can leave your money to grow into your 60s and beyond.

Yes, you do have a shorter timeline when investing in your 40s and time is not on your side to correct any wild swings or ride out the turbulence.

But it is not a good excuse to do nothing either. Unless you are sure of winning the lottery or have an inheritance coming.

So … what is investing?

Is it the same as saving?

To me, in a nutshell, saving is not spending money. Every dollar you save is one you did not spend.

And every dollar saved is a dollar that can be directed towards a goal.

Such as paying off debt – house mortgage, student loans, car, credit cards.

Or for spending later such as travel, a deposit for a house, wedding, children’s education, house renovation, retirement – there are endless ways you can spend the money you saved.

Or you can invest your savings. To me, investing is about building wealth, about growing your money. It is using your money like employees to work for you, to make more money for you. Eventually, you may spend the money invested but it is a long term, ten years or more scenario.

And it should not be at the bottom of the priority list.

Why should I invest?

Inflation.

The number one reason I invest is that I want my nest egg to beat inflation. One dollar does not buy the same things today as it did twenty years ago. And that one dollar will not buy the same things twenty, fifty years from now.

Australia enjoys a relatively low rate of inflation – currently at 1.3%. That is no guarantee that it will stay the same in the future.

So the money I save now must grow at a higher rate than 1.3%. Otherwise, I will not be able to afford the same or similar lifestyle in twenty years, as my money will have less purchasing power.

So why did I not invest earlier?

Fear.

Of losing my hard earned money.

Of doing the wrong thing, making a gigantic mistake that I cannot recover from.

Investing also implies you have money in the first place – how can you invest without money? It implies not just money but LOTS of money. And I certainly never see myself as having that kind of money.

I used to think only smart people know how to invest and that you need to know complicated investment strategies. Or that you need a financial planner or advisor.

But my biggest mistakes were inertia and contentment. Besides buying a house, I did nothing. I was happy after buying my house and did not bother with other investment opportunities.

I shoved investing into the too hard basket. And because I was time poor, I never made an effort to learn or engage a financial advisor.

How do I invest now?

When I discovered FIRE (Financially independent, retire early) blogs and podcasts, I realised there was a whole community who DIY their investment. It was empowering – it meant that I too could learn how to invest.

Now, I just keep it simple. Well, as simple as my insecurity will allow.

I automate my savings and pay myself first from every pay cheque. My system is not perfect – I will tweak dollar amounts every now and then. Once my investment account hits a certain number, I transfer it to my brokerage account to purchase shares in the stock market. More on that later.

What do I invest in?

My investment strategy encompasses three assets broadly – cash, real estate and stocks. It is not written in stone – that is I will pivot and change if needed, if for example, more evidence comes to light in regards to certain investment vehicles. Or my circumstances change.

(a) Cash

It has the lowest return on investment but I will not lose the capital, my original investment sum.

My emergency fund is in cash, in an online high interest savings account earning 2.5% currently – if I fulfill the conditions of depositing $300 per month and do not withdraw any money at all. If I break these conditions, the interest rate reverts to 1%.

I like this account because if I have to withdraw any funds, I still get 1% interest which is 10x higher than some of the accounts out there paying a 0.1% interest if I break their conditions. This cash is still readily available – I can access it from any ATM in the country.

I plan to hold my emergency fund at 6 months of living expenses – I am 85% there. Once I have reached this milestone, I will continue depositing the minimum $300 per month and build up to 1 year of living expenses, at which point I will open a term deposit account for 6 months’ of living expenses. Provided I can find a better rate.

My plan is to save 2 years of living expenses in cash. It will be my FU money. And it will guard against sequence of return risk. I will use this cash instead of selling my shares in the case that the stock market is experiencing a downturn when I finally retire.

Yes, I understand that there is opportunity costs here. I can invest this money in the stock market for a theoretical greater return on investment. But I know myself – I will sleep better at night with my strategy, knowing that I have a cash back up if the stock market crashes right at the time I retire, or just before or just after.

(b) Real estate

It was drummed into me that you must have your own home for security reasons. Especially by my mum. She grew up in rental homes and always credited her mum for having the foresight to buy a shophouse for their retirement. While my grandparents have long departed this world, that shophouse is still in the family.

A company house came with my parents’ work when I was growing up. I never lived in our own home until I was an adult after our move to Australia. So owning a home was an important goal for me. Plus I wanted to be independent and have an asset to call my own.

Many years later, I now own my home after paying off my mortgage. Now, some of you will argue that my home is not an investment, that only rental properties ie properties that generate an income should be considered an investment. Or if I have housemates paying me rent.

However, I do consider my home to be an investment because of its value to me. From now on, I live ‘rent free’ or technically ‘mortgage free’. Worrying about whether or not my rent will increase because my landlord can’t get any tax deductions or if there is a shortage of rental homes, is absent from my life. I need not be anxious that my landlord wishes to sell the property and I have to look for another roof over my head.

I absolutely acknowledge that I was fortunate and bought at a time when property prices were high but not crazy.

And yes, there are ongoing costs to owning a home – insurance, maintenance, council rates, to name a few. But my home’s value has also more than doubled since I purchased it 16 years ago. Its financial value will be actualised when I sell it to fund my move into an aged care facility or if I geo arbitrage or if I want to downsize to a smaller home. Fingers crossed, it will continue to hold its monetary value.

I list my home here only to demonstrate I have some exposure to this asset class. All money spent on the house are really just living expenses.

(c) Stock market

I invest in the stock market inside and outside my Superannuation, my retirement account.

Inside Superannuation

There are many funds within your Superannuation to choose from – the default is the Balanced fund, in most cases. This was my option ever since I started working 20 odd years ago because I never cared about retirement funds in my 20s and 30s. Now that traditional retirement is looming, never mind wanting to retire early if at all possible, I care! Very much!

My superannuation funds are now invested in low cost index funds –

My plan is to continue salary sacrificing into my superannuation ie supplementing my employer’s compulsory contribution. I will not be able to access these funds until I turn 60. If possible, I would like to delay accessing my superannuation until I am 65 or 70 to give it the best possible chance to grow.

Outside superannuation

My portfolio of shares in the stockmarket outside superannuation reflects who I am – I like variety in my daily life so I am very much into diversification. And also – remember, not all eggs in one basket? I know the stock market is one basket – but I can have different eggs just in case some of them don’t hatch. Or they can hatch at different times. (Hmmm … not sure if this analogy works!)

Nevertheless, my basket currently looks like this:

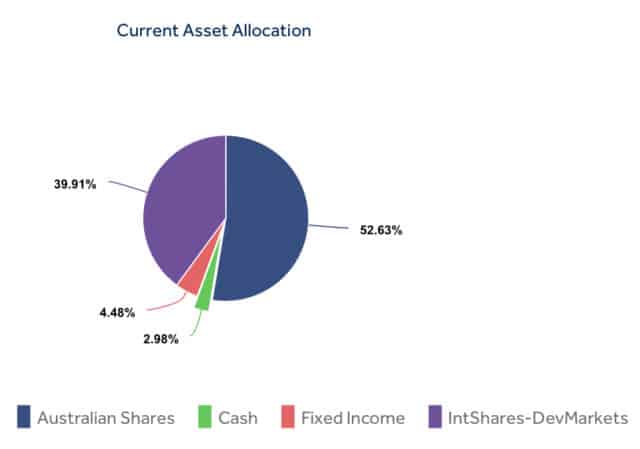

Individual shares – 44%

Listed investment companies (LICs) – 27%

Exchange traded funds (ETFs) – 29%

Individual shares

Initially, I invested in a portfolio of individual shares – 10 companies from the top 200 of the Australian Securities Exchange (ASX 200), one company in each sector. I wanted to spread my risk across all sectors so if one sector isn’t doing too well, perhaps another sector will pick up the slack. The only sector I don’t have any exposure in currently is information technology, after I sold Afterpay.

My plan is to keep these shares and participate in all their Dividend Reinvestment Plans (DRP) to very slowly build up their value. But I will not be investing new money into expanding this portfolio. Frankly, I don’t have the time to monitor each holding or research new companies to add. I am not selling any in this portfolio though as the costs of selling them and the capital gain is not advantageous to me at the moment.

Listed Investment Companies

I first learned about Listed Investment Companies (LICs) from the Barefoot Investor (affiliate link) and later from Peter Thornhill and Strong Money Australia.

These are companies that invest in other companies. And thus you are exposed to lots of companies simply by buying one share. So diversification is effectively achieved by owning one LIC.

Each LIC has its own focus eg one may own shares in the ASX200 only; another may not own any shares in the mining industry and so on.

Another thing I like about LICs is that they pay dividends. And historically, they have paid dividends even in the bad times, for example during the Global Financial Crisis. They don’t have to pay out all the dividends they receive from the companies they own all at once. And can therefore smooth out the ride in lean times.

There are currently four LICs in my portfolio. As each LIC is managed by a team who decides which company to buy and in what quantity (according to their focus), I am spreading my risk with the four LICs in the event that someone makes a less than stellar decision. I am insecure, can you tell?

Exchange Traded Funds (ETF)

An exchange traded fund is an investment fund that can be traded ie bought and sold on the stock market. They track a certain index eg the ASX200 – they are passive investments and don’t try to outperform the index it is tracking, just mimicking it. So the returns are closely tied with the index it is tracking.

For me this is the most economical way to own low cost index funds. And the best way for me to diversify my assets.

As my LICs are heavily weighted towards the ASX200, I have not bought any ETFs that track the ASX200. Instead I have one that track smaller companies (the 100 companies after the ASX200), two that track overseas markets, another that tracks Australian property trusts and a final one that tracks fixed income.

So I am quite diversified not just in the different sectors of the Australian stock exchange, but also in the different asset classes with some exposure to overseas markets. After all, Australia makes up only 2% of the global market.

I will decide each quarter which LIC or ETF to invest in, moving forward.

Final thoughts

It has taken me a while to write this post – but it has been really helpful in crystallising my thoughts on my investment strategy. I confess it sounds complicated. That is due to my insecurity and needing to diversify greatly.

I am not sure if this need for diversification is a result of my investing late in my 40s or that this insecurity is inherent in my personality and upbringing.

Please don’t let that deter you. Your strategy doesn’t have to be complicated. You just need one that works for you and allows you to sleep peacefully at night.

I am not a numbers person – I have tried to show the thinking behind my strategy – I apologise if I have confused you instead!

But I absolutely believe it is not too late to start investing in my 40s. I really don’t have any choice, with no expectation of winning any lotteries or coming into any inheritance.

Disclaimer: Nothing I write here should be considered as financial advice – these are my opinions only. How I personally manage my money may be vastly different to how you manage yours. Please seek professional financial advice should you need it.

What is your investment strategy? If you are in your 40s, how has your strategy changed? Am I needlessly diversified? Hit me with your comments below! Thank you in advance 😉

Hi Late Starter Fire, thanks for your blog, I’ve been enjoying following your journey. I wondered whether you’re factoring govt super into your numbers?

I’m a Kiwi, we currently have universal super, but I think we’ll probably end up with a means tested super like Aussie by the time I’m 65. Seems like a tough balance with means tested super – if you plan for no super you’ll end up a big enough nest egg that you wont qualify.

If you plan for super and its not there, you’ll run out of money… I’d love to hear your thoughts.

Welcome, Mr Simpleton! Do you mean our age pension? Yes, it’s means tested in Oz but I won’t be able to access that till I’m 67 whereas I can access superannuation at 60. Then yes, if I receive a pension from my super, that will affect how much I receive from the Oz government.

My way of looking at it is: superannuation is my money and when it runs out, the age pension will supplement it. If I only depend on the age pension, it may or may not be there or enough to support my retirement lifestyle. So the age pension to me is the ultimate backup – hopefully my super lasts many years before I have to rely on the age pension.

I suppose if I don’t have a choice except to rely on the age pension, then that’s ok – I can adjust my lifestyle accordingly. But I want to be financially secure so I’ll do my best to invest and save up for my future.

I think the main thing really is actually investing, once you’ve got that part done there is certainly stuff you can do to make it more or less effective but a big chunk of the work is already done.

Your investment strategy is a lot more complex than mine or at least has more going on, but it it’s what works for you then that’s fine.

My strategy has changed a bit over time from being more active to now just wanting to sit back and not have to worry about things too much. I’ve still got some legacy positions I can’t really sell off without triggering a fair amount of CGT but the aim with any new investments is to keep it nice and simple with index ETFs.

Yeah, I thought it was simple until I started to put it out there. I shouldn’t let my insecurity rule my investment strategy. But it’s basically done now – I’m just adding every quarter to each ETF/LIC in rotation as I rebalance

Kudos for getting over the fear and actually doing something. A lot of people I know have resisted doing anything more with their money than putting it in a TD or offset because of the risk that they could lose it all.

I’m all for diversification but it is also possible to be too diversified. Personally I have forgone investing in fixed income because cash is an adequate alternative, but that’s just me. You do what works for you.

We started out with an active approach but due to time constraints have moved to a more passive approach via indexes. In addition to diversifying investments I’m also planning to diversify our income streams via dividends, rental income, and Ratesetter interest.

Term deposits was exactly my parents’ strategy! Yes, only having a little in fixed income ETF as ‘insurance’ against the low interest rate for cash. The returns from that has so far been better than cash in the bank but it’s early days yet. We’ll see – happy to readjust strategy if needs be. And good point with diversifying income streams – guess I’m working on the dividend part!

Hi LSF, I’ve been enjoying your blog. Starting late is infinitely better than never starting at all. I’m a few (but not too many) years ahead of you and was also late in getting started.

Just a comment regarding investing in multiple LICs… I recall reading “Charles Schwab’s Guide to Financial Independence” a long time ago. In it Schwab discusses how diversifying via investing across multiple managed funds can result in your returns beginning to approximate the market index. Each LIC may have a specialty, but by the time you’re spread across a number of them (Schwab’s example was 10) their specialties can cancel each other out, thus approaching the performance of an index fund/etf. Investing in just a few index funds reduces the effort at tax time too.

As for me, I’m invested in VAS (21.5%), VAP (11.5%), CAM (0.5%), Growth option in a superfund (29%) and have the remaining in the US market (37.5%). I don’t regard this as ideal, but asset reallocation will incur CGT, so it is being done progressively.

Thanks so much for the info on LICs and sharing your investments. I’ve definitely capped LICs now at 4. I’ve stopped buying new stocks – I will just add to each and adjust asset allocation this way – as I too will incur CGT if I sell anything