Disclosure: Please note that I may benefit from purchases made through my affiliate links below, at no cost to you. Additionally, as an Amazon Associate, I earn from qualifying purchases

I don’t know about you, but I don’t have much will power.

For example, I want to lose weight (psst … menopause and lockdown comfort eating are not a good combo). BUT I just bought baklava and a vanilla slice from a new cafe in my local shopping centre. All I did was walk past the enticing window display and I’m done for.

The same lack of will power can apply to the money flowing out of our lives.

We know we have to start investing for that looming retirement, pay off debt and save for a longed for holiday and so on and so forth.

We know what we have to do. And yet it can be mightily difficult to execute, even though we have powerful intentions.

My answer to this lack of will power in my finances is to automate my money flow.

You make a decision once and set up the automation. You no longer need to decide each week or month if you should transfer $50 or $150 into savings.

It will automatically be done already.

Feeling Overwhelmed?

Use this FREE Checklist to start your journey to Financial Independence

Other benefits of automating your money flow

Not only do you solve the will power issue, it is so convenient once everything is set up.

You spend much less time remembering to pay the bills, or transfer money into retirement accounts or shunt money into the Christmas fund.

Because automating your money flow makes it all … well, automatic.

Even though it is automatic, you can still build in increments into your system. For example, increase your savings by 1% every month or couple of months.

The hard part is at the beginning – setting up your system, deciding which accounts to fund, how much to transfer etc

But before we get into the ‘how’, there are two principles that underpin how we manage our money.

Pay yourself first

Before I found the concept of FIRE (Financial Independence Retire Early), my money philosophy was to pay my mortgage and bills first. And then I can spend everything that is left over and save for any upcoming holidays.

After discovering FIRE, I was introduced to the principle of paying myself first.

That is, investing and saving are the first priorities followed by expenses and everything else. I had just paid off my mortgage when I found FIRE so debt was no longer an issue. Otherwise, repaying debt would be a top priority too.

The investing is for future me while the saving is for the current or the near future me (think holidays, car purchase etc)

Spend less than you earn

Step 1 - Decide on your investing and saving priorities

There are always many competing priorities for your money.

Which should you do first – pay off the mortgage, student loans, credit card or save for the holiday? How about saving for retirement?

Using the principle of paying yourself first, decide how much you want to save towards retirement, investment and an emergency fund.

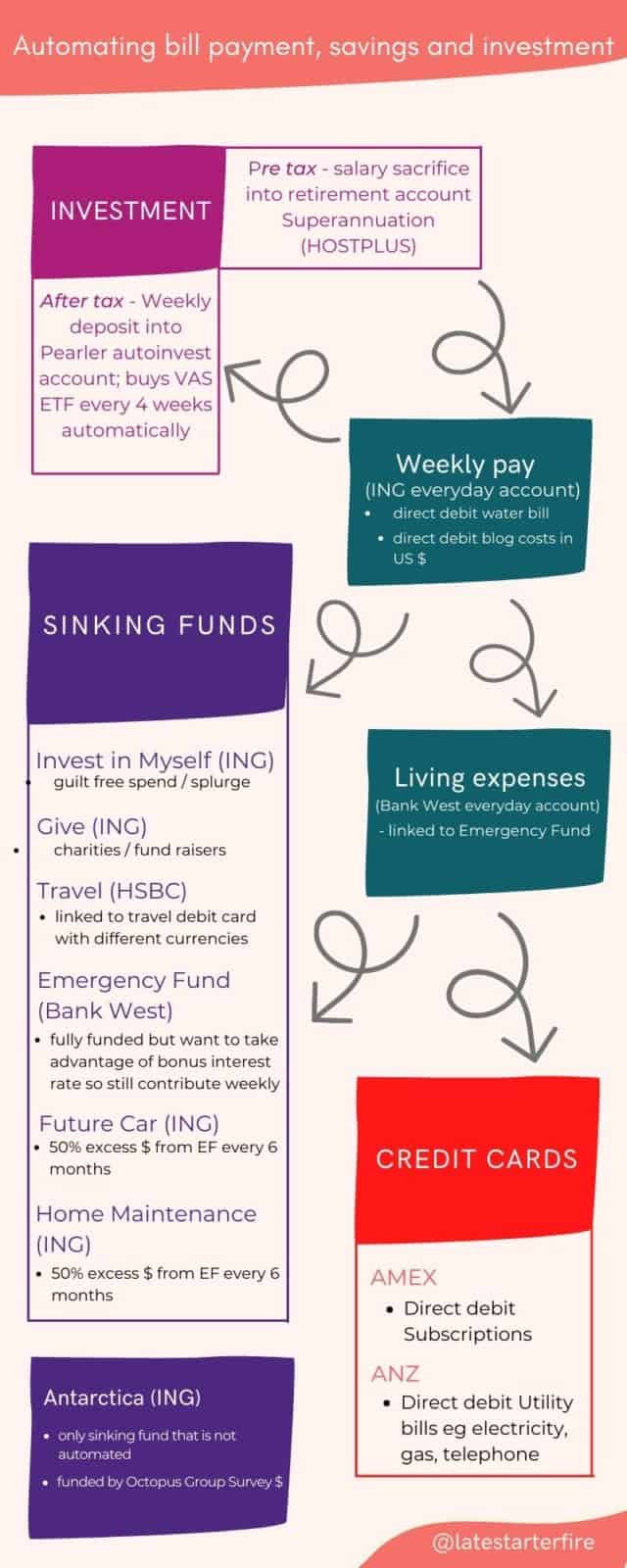

Personally I salary sacrifice a small amount towards my superannuation (retirement account) weekly from my pre tax salary. So this is automated by my employer.

Check with your HR department if they can automatically deduct a contribution from your pay and deposit it into your retirement account. And check if your empoyer has a match. If they do, make sure you’ve automated at least that percentage of your pay towards your retirement account.

Next, decide which debt you want to tackle first and how much you want to put towards various debts.

It is a juggling act at first. I like to do this on a piece of paper and adjust amounts as I factor in living expenses.

In the beginning you may not have quite enough for savings and investment but as you adjust your expenses, you will find more cash.

I encourage you to nominate a sum for savings and investment, however small to begin with; automate the transfers and then adjust later if necessary.

This is your blueprint which you’ll implement later.

Step 2 - Automate payment of recurring bills

How do you currently pay your electricity, gas, water, telephone bills?

You can arrange for bills to be automatically deducted from a credit card or directly debited from a bank account. Some suppliers even give you a discount for paying on time.

In my situation, my electricity, gas and telephone bills are automatically paid when they are due via my credit card. The water bill is directly debited from my ING everyday account. My insurances are also automatically deducted from my credit card.

Just bacause these bills are paid automatically doesn’t mean you don’t review them. I review my bills when they are emailed, just like I would if I pay them manually.

I also have recurring memberships or bills in US$ for my blog. These are debited from my ING everyday account which waives foreign exchange fees (if the eligibility criteria is met the previous month).

Therefore I make sure I leave a buffer in this account so I always have enough for all these automatic deductions.

How do you pay your credit card bill?

This too can be automated so you never have to pay interest charges in case you forget to pay on time.

It may be a bit tricky if you don’t have an everyday transaction account at the same bank. There may be paperwork to fill in – to arrange for direct debit from another institution.

Make sure you have the money in your nominated bank account when the bill is due. The easiest way is to set a reminder on your phone to double check the day before the scheduled transfer.

I must confess that I haven’t fully automated my credit card payment because I change credit cards every year or so. I semi automate the process instead.

When I receive the monthly statement, I immediately schedule a transfer from my nominated bank account. I like scheduling for it to occur a few days earlier than the due date. And set a reminder to double check there is sufficient funds in the account.

Another way is to schedule regular transfers of a set amount, for example, every week, directly into your credit card account.

Step 3 - Review and set up your bank accounts

You’ll need a primary bank account, an everyday transaction account with no fees.

Your income (salary) will be deposited into this account periodically. For me, it is every week.

And from this account, money will flow out to various other accounts such as investment, savings and any other sinking funds you’ve set up to help you save.

This part can be as simple or complicated as you like.

My setup is fairly complicated because I like my Emergency Fund to be in a different bank account (BankWest) to my everyday transaction account (ING). And preferably to be earning a higher interest rate.

I also like travelling overseas. So I have an account with another bank (HSBC) that has a debit card that can store different currencies. My travel fund is also at HSBC. it is easy for me to transfer money to the debit card account wherever I am in the world.

Decide how many accounts you need according to your lifestyle. Open new ones if needed. Nominate the purpose of each account.

A word of caution here – be aware of the hoops or rules each bank imposes in order to get a bonus interest, for example. But this is also where automation is key in helping you meet the criteria.

For example, in order for my Emergency Fund to earn bonus interest, it must grow every month without any withdrawals plus the transaction account linked to it must have $2000 deposited every month.

Therefore I schedule $500 to be deposited weekly into this account. And from this account, an amount is transferred into my Emergency Fund (even though it is fully funded). This extra amount will be transferred every 6 months to other sinking fund accounts. This means that the Emergency Fund will earn the bonus interest for 10 months of the year.

Step 4 - Set up the transfers

Now we set up all the transfers.

Log into your primary bank account (where your income is deposited). Set up weekly or fortnightly or monthly transfers – work with how often your income is deposited.

Use your blueprint with all the amounts you decided earlier.

I like to leave a day in between when money flows into an account and when it flows out of that account.

So in my case, my salary flows into my ING everyday account every Wednesday. This is the only day I feel ‘rich’, haha!

I schedule transfers to my other accounts on Thursday. These accounts include my Autoinvest account at Pearler (for investing in shares outside my superannuation retirement account), Invest in Myself fund (ING), Give fund (ING) and Living Expenses fund (BankWest).

On Friday, money will flow out of the Living Expenses Fund (BankWest) into the Emergency Fund (BankWest) and Travel Fund (HSBC)

Every 6 months, the excess money will flow out of the Emergency Fund (BankWest) into Future Car fund (ING) and Home Maintenance fund (ING).

Step 5 - Review and adjust as necessary

This is an important step.

Automating your money flow is not a set and forget strategy.

As your circumstances change, you will need to make some adjustments. For example, as you reduce your debt or expenses, you will have extra cash to invest or save towards your goals.

And as you achieve certain goals, you may want to redirect your money to new goals.

You can also anticipate this and schedule in increments to savings and investments. For example, set a goal of reducing your grocery spend over the next 3 months with the aim of saving say, an extra $100. Schedule the transfer including this $100 into a priority fund on a date 3 months away.

Or schedule a 1% increment every month.

At the very least, review your system once every 12 months.

Final thoughts

Automating your money flow makes it easy for you to pay yourself first and takes away the stress of remembering when to pay which bill.

Your system does not have to be as complicated as mine – my system works for me 🙂 Set up your system to suit your goals, priorities and lifestyle.

In summary, the 5 steps to automate your money flow are – decide on how much to invest, save and pay off debt; automate your recurring bill payments; review and set up additional bank accounts if needed; set up the automatic transfers; and review and adjust as necessary when your circumstances change or at least every 12 months.

Great post, and I feel like automation definitely eliminates any sort of self-control or discipline issues.

It might actually take more discipline/effort to prevent your automated money flow once you’ve set it up.

Reminds me of “I Will Teach You To Be Rich”‘s chapter on automating your investing, which’ll also help the investor become more ‘passive’ and not be susceptible to be influenced by Mr. Market by looking at it too much.

Reading “I Will Teach You To Be Rich’ made me tweak my money flow a little – transferring money directly into my brokerage account (Pearler Autoinvest account) and setting up an “Invest in Myself” fund. And that’s the key with automation – you still need to tweak it every now and then. And you’re right, once it’s set up, it’s passive and just works.