I don’t have a budget.

Have never budgeted.

Before or after I discovered FIRE (Financial Independence Retire Early) concepts.

I almost feel guilty writing this as having a budget is one of the ‘pillars’ of personal finance but … they just don’t work for me. So I’ll tell you about my system instead.

Please note I am not telling you not to have a budget. I’m explaining why I don’t have one. And what I do instead.

If you are struggling to stick to a budget, perhaps my way of managing my money may appeal to you. Or maybe not. Personal finance is personal after all.

What is a budget?

I like this definition from the Cambridge dictionary:

A budget is “a plan to show how much money a person or organization will earn and how much they will need or be able to spend”

That doesn’t sound too bad. I agree with having a plan for my income. And knowing how much I have to spend.

So, why don’t I have a budget then?

Unfortunately, the word ‘budget’ brings up many negative feelings in me, much like the word ‘frugal’. Although I admit I am better friends with frugal now. So perhaps it’s a matter of changing my mindset?

To me, budget screams deprivation and restrictions. And that is not attractive to me at all. I want to be free to spend my money as I see fit, thank you very much. I don’t want to be limited by some numbers on a spreadsheet (even though it would be ME putting those figures there) Can you hear the rebel in me? Sigh!

I asked a friend if he had a budget. He looked at me in horror – you mean “budget” (waving his hands in air quotes) – as in if you have $2 left in your food budget for the last week of the month, you’d eat nothing that week?

And there you have it! His reply reflects my own view of budgeting. Frankly, budgeting invokes scarcity – $2 left means I eat 2 minute noodles that week? Knowing me though, I would just take from another category and definitely still eat, no worries about that!

And if I end up stealing from Peter to pay Paul (or is it the other way round?), what is the point of diligently plugging in numbers in various categories in the first place? What is the point if I know myself well enough to know that I will not abide by those numbers?

Budgeting implies I must have strong willpower – in order to stick to the budget. I can tell you I have zero willpower. I like ice cream but refuse to have any in the house so I can’t be tempted. Then I will crave it badly, give in one night and buy two boxes. Now that my craving is satisfied, that will be the end of it. Until the next time, of course.

My money rules

Before I tell you how I manage to survive without a budget, I must tell you that I live by three rules, two of which were taught to me by my mother, from a young age. The third, I learnt as I began my FI journey.

Rule #1 – Always spend less than you earn

My mother trained as a nurse in the UK. Before leaving for the UK, she worked for a few years as a teacher in order to save up money to study overseas. Once she got to the UK, she was paid a small wage as a student nurse and lived in the nurses quarters provided.

These accommodation are closed during the term holidays so student nurses have to look for alternative lodgings. Local students could return to their homes but financially poor overseas students could not.

So my mother and her friend would save up their meagre wages and take bus trips all over Europe during the holidays. Up until dementia made her wary of travelling, she loved bus tours.

Her mantra has always been – it’s not how much you earn, it’s how much you spend; always spend less than you earn. Those student nurse wages were not much but she knew she had to save some of it to provide for the holidays or she would be homeless during the holidays.

Abiding by this one rule is my saving grace – I would be in a far worse situation now if I had not followed this rule all my life.

Yes, I definitely succumbed to lifestyle inflation as my income grew. And I had a shopping problem in my younger days. Plus I did not invest.

But I never spent more than I earned.

I can never tell you what my gross income is but I can always tell you what my net income is ie how much money lands in my bank account each week. So I always know the maximum I have to spend and I never go over that limit.

Rule #2 – Never borrow for depreciating assets, always buy what you can afford

My mother hates debt – the only debt she is okay with is to borrow money to purchase a house. Nothing else.

Her mantra has always been – buy what you can afford, never borrow money to buy what you cannot afford. Always pay in full, up front. She doesn’t like credit cards or store credit.

So I grow up to be debt averse (and risk averse too but that is another story). I never borrowed money to buy a car, furniture, appliances, holiday. I always paid off my credit cards each month. The few times when I didn’t wasn’t because I didn’t have the money. It was because I was disorganised and forgot to pay on time. Duh! I would then berate myself for paying interest needlessly.

Rule #3 – Track your expenses

I learned this rule just before I found the FIRE community and have tracked expenses for more than 2 years now. So I have data on my expenses and know what I spend my money on. Therefore I also know where I can improve upon.

But more importantly, as I manually enter my purchases later into a phone app, I think about what it is I purchased or spent on – and am reminded of why I did it in the first place. I bought that take away coffee because I was so stressed out at work. Is it a one off? Yes – I let it go. But if it’s every day? OK, that doesn’t align with my goal of reducing living expenses so why am I so stressed out in the afternoon at work?

In other words, tracking my expenses or the act of entering each transaction makes me mindful of what I spend my money on and why I spent it in the first place.

And yes, manual entering of expenses is a major pain in the backside but that is an incentive to NOT have that many transactions in the first place.

I do have a plan for my money

Even though I don’t have a formal budget as such, I do have a plan for my money.

I start by identifying my priorities or goals.

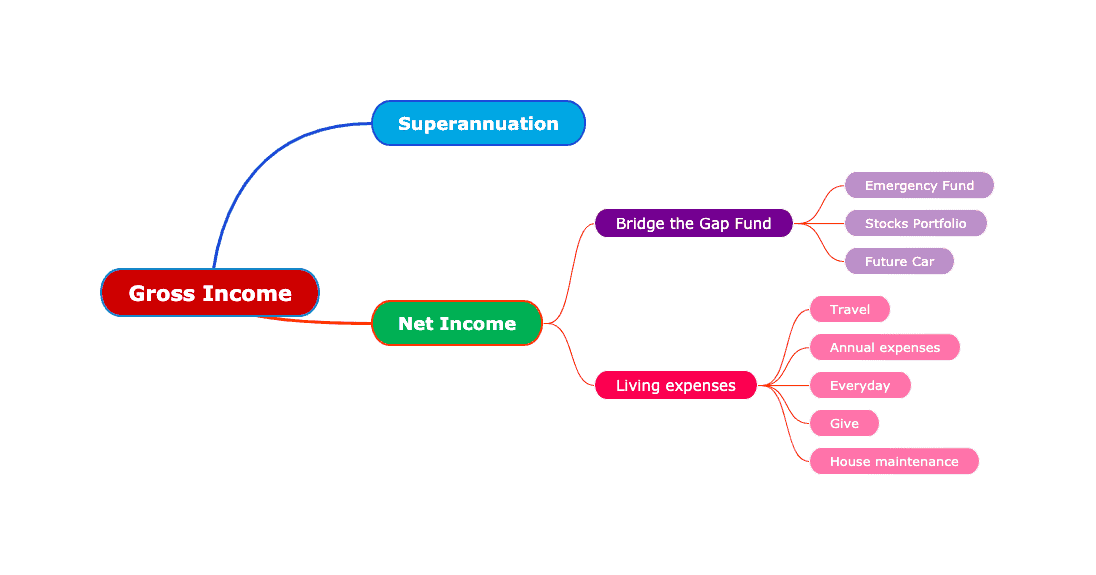

Right now, my over arching goal is to retire fully at 55. This means that I need savings to bridge the 5 year gap (between 55 and 60) until I can access my superannuation (retirement account) at 60. My superannuation also needs funding to ensure I can ride into the sunset comfortably. I am not into long arduous walks.

Therefore my income is put to work in three broad areas: Retirement savings, Bridging the gap and Living expenses.

I then look at my timeline (umm … 6 years only, gulp) and work out how much I need to direct to retirement savings and bridging the gap but still leave enough for day to day expenses. Because I track my expenses, I am not plucking random numbers out of the air.

I ‘pay myself first’ and utilise a slew of sinking funds to save for various categories. All deductions from my weekly wage (ie net income) into the various categories (or sinking funds) are done automatically. I review the amounts deducted every 3-6 months as needed.

This plan is made bearing in mind RULES #1 and #2 – always spend less than I earn and never borrow for what I cannot afford to buy.

(1) Retirement savings

(1) Retirement savings

My employer contributes 9.5% of my gross income to my superannuation. And because I am trying to play catch up, I salary sacrifice as much as I can. That is, I contribute a part of my gross wage to ensure that I contribute the maximum allowed – $25 000 annually (including my employer contribution).

So what I salary sacrifice goes directly into my superannuation – I won’t see that money until I turn 60.

As stated earlier, I never care about gross income, only what is deposited into my bank account weekly. So I don’t miss this money at all. It is gone, goodbye – off to do its job in super so I can retire comfortably one day.

And I learn to live on what is left – which is my net income.

What is left has to be sufficient for Bridging The Gap Fund and Living Expenses.

(2) Bridging The Gap Fund

To recap, I have to bridge the 5 year gap between when I retire at 55 and when I can access my superannuation at 60. Therefore this fund is invested outside of superannuation.

And is an absolute priority. Without this fund to draw on, I will not be able to retire at 55. So every spare cent counts.

This category is further divided into two buckets or sub categories – cash and stocks.

(a) Cash

My Emergency Fund is fully funded and held in a high interest savings account. I continue to deposit weekly into this account because in order to receive the bonus interest, the account balance must increase by $300 every month.

Another reason I don’t mind saving this cash is that I aim to have 2 to 3 years of expenses in cash by the time I retire – to counter sequence of risks. Just in case the stock market drops (as is happening now) at the time I retire, I will have a cash buffer to rely on and not have to crystallise my losses.

I recently opened another account – to save for a future car. Currently, I drive a work car so when I retire, I will need to buy a vehicle. As this is an anticipated need, I don’t want to draw from my Emergency Fund.

(b) Stock Portfolio

Every other available cent is directed here. I save up to $5000 and invest it in one of my LICs or ETFs.

(3) Living expenses

What is left after deductions for Bridging the Gap accounts is used for my living expenses. I further divide this sum into more accounts or sinking funds -specifically travel, annual expenses, charitable giving, everyday expenses and my latest – a fund for house maintenance. Once again, all are automatically deducted from my weekly income.

I would like to do a few things with the house before I fully retire, while I still have incoming wages. Instead of drawing on the Emergency Fund when issues arise, I can draw on the House Maintenance fund instead. It is an anticipated need so therefore I should save for it.

As I am not travelling this year, my travel fund will accumulate. I don’t have a maximum here. My rule is never to deplete it completely. I bundle this with ‘living expenses’ as I am allocating money here to be spent eventually. While the Emergency Fund gives me peace of mind should something disastrous happens, my travel fund is my happiness and freedom fund. I need to know I have money set aside to enjoy my travels without guilt.

I set up my “Give” fund last year to make it easier and more systematic to donate to charities.

The annual expenses account handles all … annual expenses such as various insurances, local council rates, professional association fees etc.

My everyday account is my last priority and deals with groceries, utility bills, gardening, hobbies etc – the day to day expenses. My goal is to reduce this as much as I can so I can redistribute it to Bridging the Gap accounts. I am currently focusing on reducing my water and gas bills.

Final thoughts

And there you have it – my money plan instead of a budget.

In summary, I adhere to 3 rules – spend less than I earn; don’t borrow to buy what I cannot afford; and track my expenses.

In addition, I automate deductions from my income directly to retirement savings and bridging the gap accounts first.

What is left over is further distributed to various sinking funds to pay for day to day living expenses. Because I am used to spending less than what I have, I am essentially tricking myself into spending only what is in my living expenses accounts.

Plus I make sure I save up for big expenses such as travel, house maintenance and a future car purchase.

This works much better for me than a budget. I don’t feel constrained as I can see my money in various accounts and draw on them as the need arises.

It is a balancing act – making sure I save enough for retirement and bridging the gap whilst having enough to live on every day without feeling deprived.

How do you budget? What is your system?

I do a broadly similar thing, plus at the end of every month I spend around 10 minutes putting my monthly spends into an annual table, so I have a running total on what my money is used for.

Thanks, Frogdancer – that is a great idea! I have a table with the total monthly expenses and compare month vs month of previous year but not broken down in various categories. Just set up new table, yes!

Funnily enough, I use and love YNAB (You Need a Budget) but I’ve also never liked budgets! Like you, I find them to be based on scarcity and too much work to adhere to.

Instead, I prefer to track my money and plan where it needs to go for future months. That way, I know exactly how much is extra and how much I can actually invest.

You’re definitely not alone with your stance on budgets!

I find that tracking my expenses make me more mindful of how I’m spending my money and therefore shows me where I can improve. And this was where I needed the most improvement

We have a fairly similar scheme to yours. All expenses are tracked, although for us it’s more downloading transactions and then sorting into categories rather than manually inputting each and every one. We track this vs what we’ve spent previously, and most of the time are fairly close to what we would expect. And we live well within our means so there are no issues with that!

Because we have a bit more of a gap to bridge between when we (hopefully) retire and being able to access our super our focus is moreso on our investments outside super once we’ve maxed out the tax savings that super offers.

So on the investing side I salary sacrifice up to the $25,000 limit, and put in $3,000 as a spouse contribution for my wife. Everything else gets invested whenever we get to a worthwhile amount, normally $4,000 or so.

That is the only advantage starting later has – we need to save less to bridge the gap to when we can access super!

The tax benefits of super is hard to ignore – my accountant wants me to invest more in super as non concessional contribution. He doesn’t understand that I want to retire at 55.

We did like you, bought cars and other consumer items with cash, paid the house off early and lived frugally and maxed out all retirement vehicles and regular savings and built taxable brokerage accounts with what was left over. We eliminated education costs for our kids with public schooling and encouraged them to find scholarships that paid 100% of their four year degree costs including room and board. We were a single income family but as my career advanced it became a very large income.

We had plenty invested to bridge the gap but to keep my brain sharp I decided to consult a day a week after retiring and that ended up fully funding our $100K living expenses. In fact we’ll delay Social Security until we hit 70 because we don’t need the money. We won’t need it then either but we paid for it so we’ll certainly take it.

Living below my means has certainly set me up for the future but wish I had focused on investing much earlier or paid off my mortgage earlier but then again, I don’t regret travelling either.

It’s amazing that working one day a week is enough to fund your $100K lifestyle!

Like you, ‘budget’ evokes negative feelings – I was on a strict budget when I was paying down my debts so it’s not something I want to do again, even if it’s for something positive like aiming for FIRE.

I hear you! Once our big goals are achieved, we can ease back a little and not be so strict! Gotta enjoy life as we proceed to FIRE

I’m terrible at tracking my expenses, so I use a fuss-free method to ensure I don’t go overboard with my budget. Basically, I give myself a certain budget to spend each day. It doesn’t matter what I spend but s long as I don’t go over that amount. True, I think budgets tend to make me feel a wee deprived, but over the years I’ve made them fun. I occasionally participate in no-spend challenges just to see if I could do it. It’s turn out to be quite fun.

Yes, I occasionally do no spend challenges too though training myself to be mindful of what I spend on is probably the most effective technique to reduce my spending.

I started tracking expenses to see what my saving rate was – and because I wanted to beat it each month, I continued and now it’s a habit.

I do want to start tracking my expenses. So that I can optimise my savings/expenses better, but I can’t seem to do it! ;D But I’m not kidding when I say I’m absolutely hopeless at it. I will collect all receipts only to forget where I put them. I would dutifully track using an app for two days then forget to do it for weeks. It’s almost as if my brain rebels at the idea of imposing some kind of order to my expenditure. Rather than fight it, I’ve decided to work with it and it’s been okay so far. 😛

Do what works for you!

My method for tracking my expenses – I record immediately on an app on my phone if I use cash, otherwise I keep receipts in my purse and record all at once, either weekly, fortnightly or until I have a stack of receipts. Plus go through my electronic transactions at the same time. I try to do it at least twice a month so it’s not so onerous at the end of the month.

I have been known to avoid this task if I feel guilty or know it’s going to be a bad month

Great Post!

I have a confession – I preach about the ‘virtues’ of having a budget but to be fair I don’t use my budget in the traditional sense.

Firstly, I use my budget more as a means of tracking expenses, just lie your rule #3.

Secondly, I use it as a way of extending the gap between what I earn and what I spend.

Once I have locked down things like ‘fixed’ living expenses (mortgage, utilities, internet) and savings, the rest of the money is there to do what I want with – I give my self an allowance.

From my allowance, I can choose to buy enough groceries to feed me during the week and not go out, or I can choose to eat out every day and not cook at home,

Of course, in practice, I do a mixture of both, but either way, as soon as my allowance runs out, I need to stop spending.

The reality is, there is always tons of food in my fridge, freezer and pantry, so I never have to worry when my allowance runs out.

Even though I know there are some at the frugal end of the FIRE community who brag about running out of the last morsel of food right before their weekly scheduled shop, and then buy only enough to last them to the next shop. Agggh – that would drive me nuts.

I think that you have hit the nail on the head though – you need to know your values about money and your life goals. The rest should figure itself out.

Using a budget just helps you to validate your gut feelings about your values, and ensure that you reach our goals.

Thanks for giving us an insight into how you ‘budget’.

Shaun

I like your idea of an allowance 🙂 though it includes food? Not sure how I would cope with that, haha – as after fixed expenses of utilities, insurances etc, food is the one expense I really enjoy spending on … Like you, I always have enough food in the fridge, freezer and pantry but do like to treat myself once in a while to say, good cheese or a cooking class

If budgeting doesn’t suit you, have you looked into Conscious Spending before? It’s something, I believe, Ramit Sethi coined… Basically you’re starting from zero and simply adding what you WANT to spend, rather than working from a fixed budget amount. In this way, you’d add the things you really want to have/value, first (being honest about it, too!), then add in your fixed expenses like rent, bills, etc. You’d wind up at the end with a total cost to incorporate everything into your life that also fulfills your wants.

Then you work towards that income.

It’s an interesting idea for folks where budgeting seems kind of pointless. 🙂

Cheers!

You are the second person to mention this! Will definitely look into it. Sounds intriguing

Congrats on the feature in PFB this morning. Great article. I am similar to you, no hard set budget. I prioritize putting money into investments, and spending less than I earn, but no hard set budget.

Thank you, Andrew! I’m a big proponent of ‘do what works’ so if we are still saving for our future and spend less than we earn then we’re good! I hate feeling constrained 🙂

You have to do what works for you. It sounds like not having a budget is working! I never had a budget per say either, and then I tried You Need a Budget (YNAB) and it changed my life. Having the budget didn’t change my life, but the way it syncs with credit cards and shows where money is going and coming from made me realize how much I was actually spending each month on certain items and how poorly I was doing actually tracking that spending. It has also helped me plan bigger expenditures too. I love YNAB. LOL!

That being said, I don’t adhere to a strict budget. If I go over my “Eating Out” allotted amount each month, I just add more to it from my allotted grocery amount. No deprivation for me. HAHA! 🙂

It sounds like you are killing it with all your savings goals, so I say keep doing you!

I hear so many good things about YNAB – if I ever try a budget tool, I think it’ll have to be YNAB!

No deprivation for me either! Ha ha!

We all just need to do what works for us 🙂

We tried a hard budget for a few years but it didn’t seem to work for us either. I think that tracking your expenses and being mindful of your spending is much more important.

You’ve got a well thought out money plan – I wouldn’t be too worried about the lack of “budget.”

Thanks, Maria – glad there’s more than just me out there who don’t like hard budgeting!

I’m much more gung-ho about budgeting and planning! The thing is, I don’t see my budget as a way to ‘restrict’ myself. It’s a budget but more primarily it’s also a tracker. And it’s a way for me to see how lifestyle inflation is affecting me.

Take food for instance. Takeaway food is a massive weakness in my budget. I acknowledged that when I first created my budget, but did I restrict my eating out? No, I set the budget amount at $200 per month and built the rest of my budget around that, acknowledging that I spend that amount. But, having that number budgeted in allows me to see when I’m letting myself get slack — after getting home from my holiday in March this year, I found that my monthly takeout bill was over $400! And this was WITH lock down and not having any social engagements to go to. This is where the budget comes in useful, as from August onwards I have revised my target downwards and mentally set myself the challenge of sticking to a hard limit for eating out this year. If I can be good and stick to the rules this year I’ll see about loosening it back to $200 in the new year.

Having my rolling budget also lets me look back on previous years and see what other costs are changing – insurance premiums, for one! Income protection insurance is being hiked by a massive 50% this September – ouch!

It’s really about mindful spending, isn’t it? Once you are aware of your spending pattern, it is easier to tackle and put in strategies to cope with it. During this pandemic, I don’t there is anyone who hasn’t eaten more than before. We must be seeking some comfort in this turbulent time.

I honestly tried full on zero based budgeting and wasted so much time figuring everything out into neat little columns and rows and categories on excel and then… didn’t really stick to it HAHA. I’m crap at budgeting, but I’m good at tracking my expenses, being frugal and paying myself first (investing at the start of the month). I guess we all have our different systems

I think zero based budgeting may be easier with a budgeting program eg YNAB rather than doing on excel – it would drive me nuts. But I love tracking my expenses on a spreadsheet. Totally agree that we just need to do what works for us